Talking to cap intro people is like going on a first date. You know there are (potential) interests from both sides, and even though you both want (more or less) the same thing, you never know if there’s going to be a second date. But once in a while, you come across someone just *gets* you.

Fundraising for a value investor is like that, with a slight caveat: It’s more like competing for attention in the large pool of hot, young hedge funders.

This all changed last week, when we had a particular exhilarating conversation with a cap intro group. The good (and sometimes, bad)thing about being a value investor, is that when people get it. THEY GET IT. Often time, a question is asked so naturally, and so ahead of a presentation, you end up jumping through the conversations: One ends up wanting to continue, despite running over the original meeting time.

And one of the topics that people either buy in with enthusiasm, or shy away like a bad smell, is the idea of concentration. And why is that?

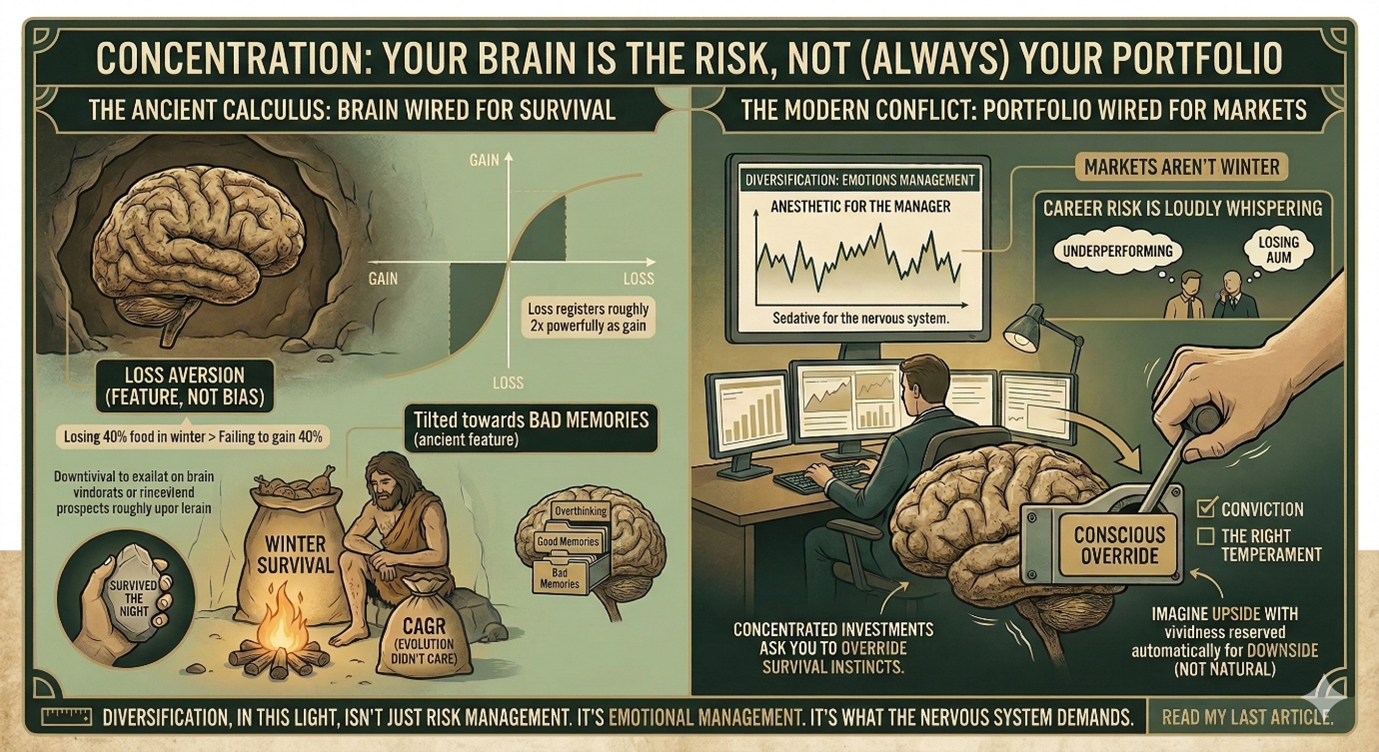

It's not a portfolio decision. It's a psychological one.

The human brain isn't wired for concentration. It's wired for survival. Loss aversion isn't a bias we need to correct, but a feature that kept our ancestors alive. And it’s true, by the way: Losing 40% of your food supply in winter is not the same as failing to gain 40% more. The asymmetry was real, and it’s also the cornerstone of “Prospect Theory”: Evolution didn't care about your CAGR; it cared about whether you survived the night.

Just ask anyone who tends to overthink, they will tell you the tendency is always tilted towards the bad memories, and not the good ones. I still haven't forgotten a cross-Atlantic red-eye next to a screaming toddler. Then again, it's harder to forget when the toddler is yours.

The problem is that markets aren't winter. And yet we carry the same ancient calculus into the portfolio: where the pain of a loss registers roughly twice as powerfully as the pleasure of an equivalent gain, especially when career risk is loudly whispering at the back of one’s mind. Diversification, in this light, isn't just risk management. It's emotions management: It's what the nervous system demands.

Concentrated investments ask you to override that. To imagine the upside with the same vividness that the brain reserves, automatically, for the downside. And that is definitely not natural: it is a conscious choice. A choice backed not only by conviction, but also the right temperament.

When it goes wrong, the wiring wins… LOUDLY

The most famous concentrated bet on Sears is, of course, Eddie Lampert's. He orchestrated the Kmart-Sears merger in 2005 and ran the combined entity forever a decade. What most people don't know is that Lampert probably came out fine. Through dividends, spin-offs, interest payments, and roughly $2 billion in performance fees earned during the stock's rise, his net position on Sears appears to have been profitable, even after the 2018 bankruptcy. His real fortune was made elsewhere: a 30% stake in AutoZone, bought around $20 per share in 1997 and exited between $500 and $600 for approximately $1.5 billion .The opportunity cost of the Sears years was enormous, but Lampert is still a billionaire.

Our focus, though, is on someone who came in later and bet the farm. Baker Street Capital, and it’s something we still discuss internally from time to time.

In 2013, they commissioned a property-by-property appraisal of Sears' top 350 owned and 50 leased locations, valued the real estate alone at $7.3B, and published a 139-page pitch deck arguing that Sears traded at one-third of its breakup value, with upside ranging from 92% to 258%. It was one of the most thorough sum-of-the-parts analyses of that era. The kind of work that makes a lot of people nod along and think, “Yes, that’s obvious”.

Then reality moved in two directions at once. The model faced two headwinds that proved decisive: $5B+ in pension obligations that weighed heavily on any restructuring, and a set of catalysts that simply didn't fire in time. The Lands' End spin-off, Sears Canada, the REIT structure, each was a plausible path to unlocking value, and each fell short of what the thesis required. Meanwhile, retail losses don't pause while asset monetization plays out. Quite the opposite actually: they accelerate.

The assets were real. The process was sound. But concentration meant there was no margin for the two things that weren't in the model: the liabilities that were buried, and the catalysts that never came. It also amplified everything: the conviction, the commitment, and ultimately, the loss.

After Sears filed for bankruptcy in 2018, Forbes ran the headline: "The 34-Year-Old Hedge Fund Manager Who Bet Everything On A Stock That Tanked." And THAT became the cautionary tale that allocators quietly cite when you mention 10 to15 positions.

The thing is that concentration isn’t inherently good or bad; it’s a double‑edged sword that can either magnify returns or speed up losses. Besides having strong conviction, perhaps more importantly, one needs to make sure there is sufficient margin of safety in catalysts. Ultimately, it all comes down to one thing: the quality of the assumptions you’re standing on.

We constantly remind ourselves internally: The quality of the investment begins with airtight assumptions. And that is the difference between building on bedrock or quicksand.

And when it goes well… It goes REALLY well.

But the wiring can work the other way too.

The same nervous system that screams sell at the wrong moment can, in the right hands, become a contrarian instrument. When markets are panic selling, the concentrated investor who has trained themselves to feel the upside (not just imagine it, but viscerally feel it),can move toward the fire while everyone else runs.

Not out of recklessness. Out of preparation.

That's what happened in 2011, in a corner of the credit markets that most equity investors never look at. And this one, I find it genuinely fascinating.

Our CIO, Shaun Heelan, recalled after the GFC, the BIS changed the capital rules for CMBS mezzanine bonds. Overnight. An originally rated AA - BBB bond that gave banks a 156% ROE in July 2011 suddenly required 100% capital deduction: collapsing that ROE to 2.5%. The bonds didn't get worse. The rules changed. And that was enough.

Banks and many insurance companies had no choice but to sell. A tidal wave of forced sellers, into a market with almost no buyers. Bonds that traded at 60 - 85% of par in spring were at 4 - 8% of par by autumn. Yields north of 130%.

Most investors saw the headline and ran .Interest shortfalls. Delinquencies. Names still carrying the bruises from 2008.Completely understandable: that's exactly what the nervous system is designed to do.

But the mechanics told a completely different story. Unpaid coupons accrued. When a mortgage liquidated, junior bonds got paid before senior principal. Years of missed coupons has the potential to recoup in a single month.

Modern day cigar butts, hiding in plain sight.

And here’s the nuance I love: while many insurers were pushed into selling by new capital rules, a subset of large, well‑capitalized life companies did the opposite. They used the new, model‑based regime to their advantage: selectively buying deeply discounted CMBS and RMBS where expected losses were small relative to price, locking in equity‑like returns inside supposedly “boring” balance sheets.

The few managers and institutions who understood the structure, did the work, and had the conviction to concentrate? They bought billions of face value at single‑digit dollar prices and made multiples of their original investment.

That's not luck. That's what happens when preparation, process, and psychological discipline converge at exactly the moment everyone else's nervous system is screaming sell.

--Jenny Ngan , Head of Business Development