I had an interesting conversation with an allocator recently. And I mean interesting in the way that a good puzzle is interesting: not because it annoyed me, but because it said something true about how this industry thinks.

He asked whether we use leverage. The answer is no. And he seemed, genuinely, a little disappointed. Like someone had invited him to a fireworks show and handed him a sparkler.

Then I told him we run a concentrated portfolio. 10 to 25 names. European SMID-cap. High conviction. The response? Something close to alarm. "Wow, that's a lot of risk."

I made a mental note to come back to this. Because here is the thing: both tools do exactly the same job: They amplify.

Leverage amplifies using borrowed money. Concentration amplifies using position sizing.

The intent is identical. The mechanics are different. And yet one gets a nod of approval, and the other gets a raised eyebrow.

That asymmetry in reaction is worth exploring more.

Personally? I don't think it's purely rational. But I've had to reckon with the fact that it is not entirely irrational either.

And the difference matters.

The Amplifier Question

Let's be honest about what both tools are doing.

Leverage takes your capital base and multiplies it with debt. If you have 100 and borrow 200, you now have 300 at work. A 10% move becomes a 30% gain or loss. The amplification is real, mathematical, and external: you borrowed from someone else to make it happen.

Concentration works differently. You don't borrow anything. But instead of spreading your 100 across 50 positions at 2% each, you put 15% into your best idea, 12% into your second, and so on (ok fine, we will concentrate HEAVILY when we see the asymmetric risk/reward, but I digress).

The amplification comes not from leverage but from conviction expressed through sizing. It is internal. And it lives or dies on the quality of the JUDGEMENT behind it.

The allocator who approved of leverage but flinched at concentration was, without realising it, saying:

I'm more comfortable with borrowed money than I am with confident judgment.

<Insert pause and repeat>: I'm more comfortable with borrowed money than I am with confident judgment.

What a fascinating thing to be more comfortable with. Or so I thought. Because when I became curious and decided to dig deeper, I discovered… He actually had a point.

… Just not the one he intended.

The Case for Leverage (Made Honestly)

When I brought up this topic with our CIO, Shaun, and head of research, Rahul, we started to understand what the sophisticated allocator actually knows, and what the simple 'leverage bad, concentration good' framing gets wrong.

Rahul brought up a really good point here: in the modern institutional world, leverage in a well-structured fund is tightly bounded. A pod shop running a market-neutral book operates with hard stop losses, typically in a narrow band. When the position hits the stop, capital is redeemed. The LP does not lose more than the stop loss allows. The prime broker enforces it. The structure works as designed. This is not a theory. It is the daily operating reality of the multi-strategy world.

And the systemic risk of LTCM-style leverage (25-to-1 on correlated positions) is structurally impossible in the post-GFC world. Basel III and IV counterparty capital requirements, mandatory clearing, and prime broker exposure limits mean that kind of leverage cannot be assembled the same way. The regulatory changes after 2008 were precisely designed to prevent it. So using LTCM as a live warning about modern leverage is, if we are being honest, historically unfair.

As for Archegos Capital: yes, it blew up spectacularly in March 2021. But it was not a representative leverage failure. Bill Hwang was running directional leverage, not market-neutral, using total return swaps to hide concentrated exposure across multiple prime brokers simultaneously, at a firm with a prior fraud conviction, on a book that was largely his own capital. Archegos is famous precisely because it was an exception: a compounded failure of opacity, alignment, and regulatory evasion that happened to involve leverage.

It is not the cautionary tale about leverage in general. It is the cautionary tale about what happens when the rules designed to bound leverage are deliberately circumvented.

So the allocator who nods at leverage is not being naive. In the modern institutional structure, a pod shop's stop loss is a real, enforceable cap on LP losses. That is a genuine form of downside protection. And it deserves to be acknowledged as such.

The Historic Antidote: Why We Keep LTCM in the Room

And yet.

We keep Long-Term Capital Management in the conversation not as a warning about what leverage routinely does, but as a reminder of what leverage can do when the assumptions underneath it break all at once. Their positions were, in isolation, defensible. What the models could not account for was the moment when correlated positions became perfectly correlated, when liquidity vanished, and when the margin calls arrived simultaneously across the entire book.

The Fed had to orchestrate a private-sector bailout. Not because LTCM's losses were uniquely large, but because the counterparty exposure was so entangled with the major banks that an uncontrolled unwind threatened the broader system. That is the feature of leveraged structures that stop losses do not address: systemic contagion. A stop loss protects the LP. It does not protect the prime broker, the counterparty, or the institution on the other side of the swap.

The pod shop model survives idiosyncratic risk beautifully. One position blows up, the stop fires, capital is redeemed, the PM is dismissed, the book moves on. But the pod shop model's existential risk is exactly what the counter-argument acknowledges: a freeze in prime broker funding. March 2020. March 2008. These are moments when market-neutral correlations converged to 1 and funding evaporated simultaneously. In those moments, the stop loss is not the binding constraint. The prime broker's balance sheet is. And a concentrated long-only fund has no prime broker to freeze it.

LTCM, in this sense, is not a warning about leverage in 2024. It is a warning about what happens when the structure that bounds leverage: counterparty diversification, liquidity assumptions, correlation models, fails to hold. That warning does not expire. It just waits for the next version of the same mistake.

The Stop Loss That Saves You. And Closes the Door.

Here is the concession we are willing to make, and the argument we want to make from inside it.

A stop loss is real protection. It caps LP losses. It forces discipline. In a leveraged market-neutral structure, it works. I accept all of that.

But a stop loss is also a cap on recovery. The moment the stop fires and capital is redeemed, that LP's money leaves the strategy. The position that was down 15% and would have recovered to flat, and then to a 30% gain, never gets to prove it.

The LP gets their capital back, minus the loss, and starts again. The stop loss that protected them from losing more also prevented them from getting back what they lost.

This is not a theoretical concern. The managers who have built the best long-term records in concentrated value investing (Klarman, Gayner, Armitage) have all held through drawdowns that would have triggered a stop loss in a leveraged structure.

The 35% drawdown that looks catastrophic in quarter three is the entry point for the position that doubles in year two. That recovery path is structurally available to the concentrated long-only investor. It is structurally unavailable to the investor whose capital was redeemed at the stop.

So the question is not which structure loses less. The question is: whose problem is the failure, and does the investor retain the option to recover from it?

In a leveraged structure with a stop loss: the LP is protected, the recovery path is closed, and the PM starts over.

In a concentrated long-only structure: the LP absorbs the drawdown, the recovery path stays open, and the PM can hold. Whether they should is a different question entirely. And it is the most important one.

The Risk We Don't Talk About: The Trader Option

This is the part where I have to be honest about the real danger in a concentrated book. And it is not the one most people point to.

When a concentrated PM is down 30 to 40%, something happens to the incentive structure. The expected value of disciplined loss management (trimming, updating the thesis, accepting the loss) is a job at risk. The expected value of taking more risk to get back to flat is, mathematically, the only play that keeps the career alive. This is what options theory calls the trader option:

The asymmetry between the PM's upside (performance fees, career preservation) and the LP's downside (permanent capital loss) creates an incentive to reach for risk at exactly the moment when risk should be reduced.

And unlike a margin call, no one forces them to stop. There is no prime broker on the phone. There is no stop loss hardwired into the structure. There is only the PM's judgment, under enormous pressure, at the moment when judgment is most likely to fail.

This is a genuine, documented, and underweighted risk in concentrated vehicles. And I raise it here because ignoring it would make everything else I've said about concentration less credible, not more.

It is also, not coincidentally, precisely why our modified Kelly framework and the Arch exist at MAAT.

Our modified Kelly-based sizing framework does not ask "how much do I believe in this?" It asks: given the edge, the downside risk, and the correlation to everything else in the portfolio, how much capital does this deserve right now?

The question is answered mathematically, not emotionally.

And as the risk/reward of a position deteriorates, as a loss deepens, as the thesis weakens, the framework mechanically reduces the position. The PM cannot rationally justify doubling down because the framework makes the case against it in numbers, not feelings.

The trader option is the concentrated PM's equivalent of the margin call.

The difference is that the margin call is imposed by the structure. We have built the discipline into the process, so it does not need to be imposed from outside.

The Volatility Confusion

There is one more layer to this. And it explains the allocator's reaction as well as anything.

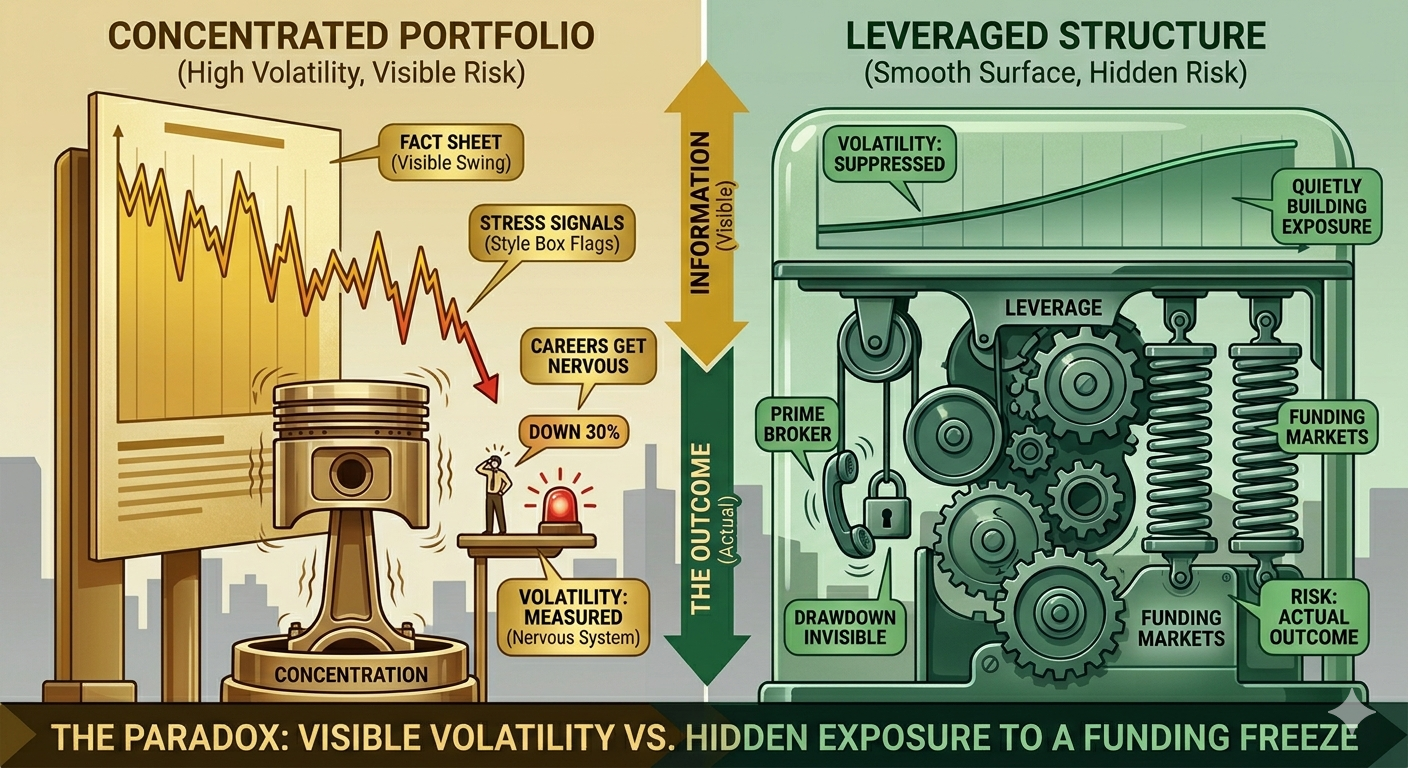

Most people confuse risk with volatility. And once you have made that confusion, concentration looks riskier than leverage because a concentrated portfolio swings more visibly against its benchmark. One position down 30% moves the whole portfolio. It shows up in the fact sheet. It triggers style box flags. Consultants notice. Careers get nervous.

Leverage in a market-neutral structure is smoother on the surface: the volatility is suppressed, right up until the moment it isn't. The event is not a bad quarter. It is a prime broker on the phone, or a funding market that has seized.

Volatility is what the nervous system measures. Risk is what the outcome actually is.

They are related, but they are not the same thing. And our industry has spent fifty years optimising for the former while calling it the latter. The stop loss that bounds LP losses also bounds LP visibility into what is really happening. The drawdown that is visible in a concentrated fund's fact sheet is, paradoxically, more information than the smooth returns of a leveraged structure that is quietly building exposure to a funding freeze.

What We'd Rather Amplify

At MAAT, our decision not to use leverage is not a timid one. It is a structural one. And it comes with an honest acknowledgement of what we are taking on instead.

We are taking on visible volatility. We are taking on the risk that a concentrated position moves against us and that the LP sees it in real time. We are taking on the responsibility of holding through drawdowns without a structural mechanism that forces us to stop. And we are taking on the discipline of ensuring that the trader option, the temptation to reach for risk to recover losses, is addressed not by a prime broker, but by a framework.

In exchange, we retain the recovery path. We retain the ability to hold the position that is down 35% in October and potentially up 80% by the following December (illustrative, not a return projection). We retain full transparency: Our LPs can see every position, every size, every thesis. There is no opacity, no hidden swap exposure, no prime broker whose balance sheet we depend on.

The portfolio is designed to distribute stress, not absorb it (I wrote about this topic here). We call this the Arch. When one position moves against us, the structure adjusts. Not in a panic. Not because a prime broker called.

Systematically, and on our own timeline.

That, in my opinion, is the harder thing to build. And relying, heavily, on judgement. And discipline. And the deep understanding of, not only limited to our positions but rather, our psychological tendencies more than anything else. The ability to stay disciplined, as a team, to do what we're saying to do. And to trust that our system is sound.

It's true... in our opinion, the most dangerous amplifier is not the one that fails most spectacularly. It's the one that removes your ability to recover from the failure. Choose your amplifier carefully. Because you are also choosing which door closes when it goes wrong.

The allocator who approved of leverage because he could audit it, and feared concentration because he couldn't, had confused the measuring stick for the thing being measured. Binet would have recognised the error immediately. And in the words of Mark Twain, which our CIO Shaun Heelan comes back more than any other:

"It Ain't What You Don't Know That Gets You Into Trouble. It's What You Know For Sure That Just Ain't So."

-Jenny Ngan , Head of Business Development

Disclaimer: This post is for informational and educational purposes only and does not constitute investment advice or a solicitation.