Like many, during Covid when there was little to look forward to, I found solace in an unusual place. The TV show and eponymous character, Ted Lasso. Quite to my surprise, apart from being entertaining and funny, it came to be inspiring and educational. From it I found a new favorite quote: “Be curious, and not judgmental”. Indeed, it was my guiding principle when I ran for the supervisory board position at my kids’ school. It has become a motto for my life in general (just ask my two boys!). And I know I’m not the only one.

In my last post (if you missed it, it’s the one about concentration and why it makes allocators either lean in or run for the door), I mentioned Thomas Gayner and teased that there was more to say about him. That he wasn’t really a concentration story. He was a curiosity story.

Here’s what I mean.

The “cool” thing about Value Investing…

To no one’s surprise, value investors tend to adopt a contrasting perspective from other investors. The nature of that contrast varies. They may have an alternative angle, a unique interpretation, or just in general, “see” it differently. And that extends to how we evaluate a business. Most people look at revenue, margins, EBITDA, the whole shebang (all useful, by the way). True value investors tend to go deeper and find things beneath the surface.

Staying true to the value investing concept: Nothing comes easy (ain’t that the truth). It’s not a number you can find on Bloomberg. Buffett called it “owner earnings”: The cash a business actually generates for its owners after you strip out the maintenance capex needed to keep the lights on. Not the reported number. Not the adjusted number. The real number: what’s actually left over for the person who controls the check book to deploy (in this household, it’s me, for what it’s worth). And you have to calculate it yourself. But that’s what makes it so valuable, because the calculation forces you to truly understand the business – as an owner would. Is that capex maintenance or growth? Is that acquisition creating value or destroying it? Is that buyback happening because the stock is genuinely undervalued, or because the business has run out of reinvestment runway?

These are beautiful questions. They’re the questions that turn a stock into a business in your mind. And every dollar of owner earnings faces a decision: Reinvest in existing operations? Acquire something new? Buy back shares? Pay down debts? Pay a dividend? Sit in cash and wait? The answer to that question, repeated over years and decades, is the single biggest driver of whether a company compounds. And when a CEO gets this right – and I mean really right – the results are equally beautiful.

Dr. George Athanassakos, the Ben Graham Chair at Ivey Business School, has spent years studying exactly this. In his 2024 paper “Do CEOs Identified as Value Investors Outperform Those Who Are Not?” (Journal of Risk and Financial Management), he found that companies run by CEOs who deploy cash flows in a value-investing style significantly outperform those that don’t: by an average of 33% in cumulative three-year returns. In other words, the difference between a great CEO and a legendary one comes down to one pivot mindset: what to do with the remaining cash.

Prof. Athanassakos writes: “The best CEOs are those who are good value creators, as well as good value seekers. To be a good value seeker, the CEO must be a good investor, more importantly, a value investor.”

Read that again. He’s saying the skill of running a business and the skill of investing in businesses are, at their core, the same skill. The best operators are also the best allocators. And the best investors? They recognize this, and they do it themselves.

Ask not only if the business makes money, but what to do with the money it makes.

The Man Who’s Good at Both

This is where Thomas Gayner becomes fascinating. And why I said his story was a curiosity story, not a concentration story.

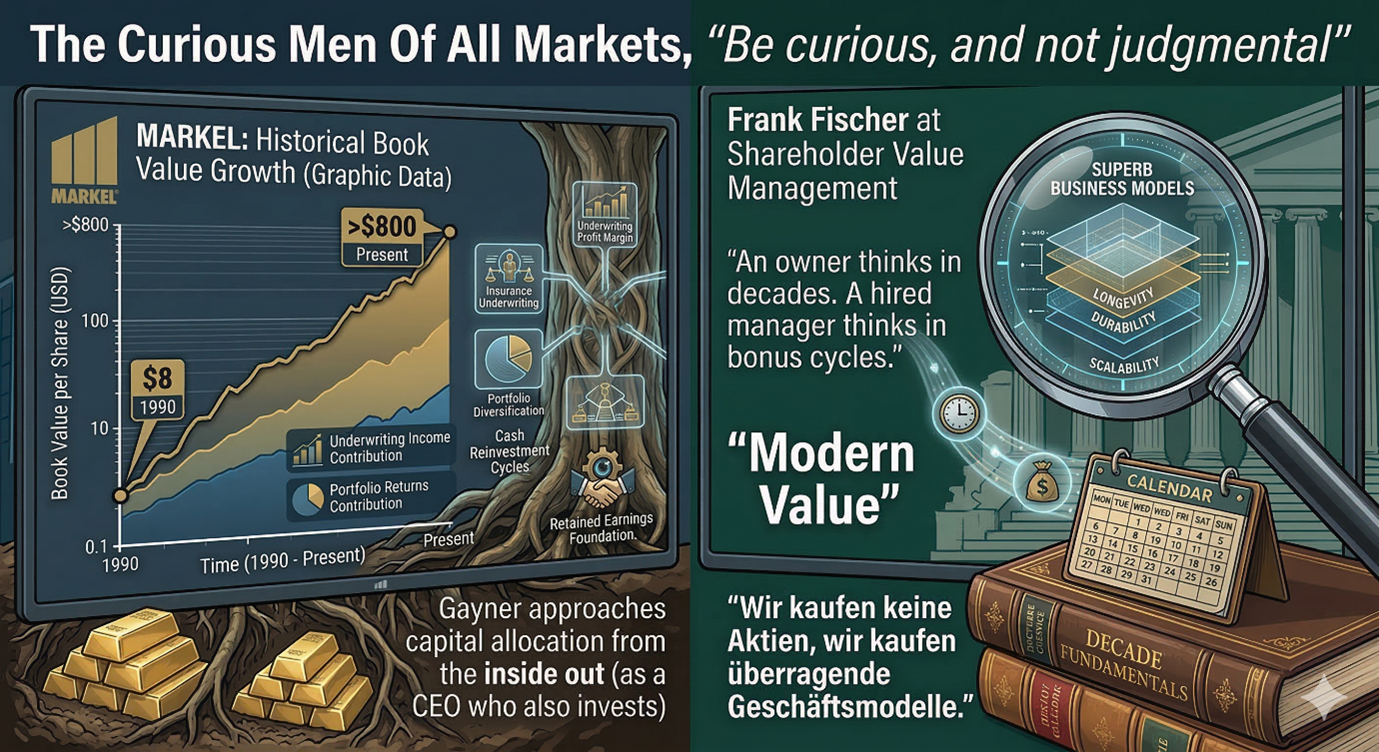

Gayner is the CEO of Markel Group, a Fortune 500 company often called “baby Berkshire.” When he joined in 1990, the book value per share was $8. Today it’s north of $800 (yes, read that again – eight hundred). And he has done it by being, simultaneously, a capital allocator inside a business and an investor outside in public markets. He lives on both sides of the mirror and excels at it.

At Markel, Gayner describes having what he calls a “360-degree view” of capital allocation (not dissimilar to the 360 employee reviews we used to do at Goldman, by the way). He has laid out his priorities explicitly, and the order matters: First, fund the businesses you already own – the proven winners inside the tent. Second, acquire new platforms. Third, buy publicly traded securities. Fourth, buy back your own stock. That hierarchy tells you everything about how he thinks. Existing businesses first. New opportunities second. Public markets third. Buybacks last. Not because buybacks are bad, but because they should only happen when nothing better is available.

When he was asked which of his four investment criteria matters most – 1) profitability, 2) management integrity, 3) reinvestment dynamics, 4) fair price – he didn’t hesitate. It’s reinvestment dynamics and capital discipline. Because, as he put it, that criterion embeds all the others: if the business isn’t profitable, there’s nothing to reinvest. If management isn’t honest, they’ll steal it.

And here’s the line I keep coming back to. Gayner says Markel would be lucky to find two or three businesses run by great capital allocators in any given year. Two or three. Out of the entire public market. That’s not a stock-picking problem. That’s a human capital problem. Most CEOs simply aren’t good at this. And the investors who can recognize the ones who are? They tend to be great capital allocators themselves.

Gayner made exactly this point in an interview: his experience in equity markets makes him a better judge of how companies allocate capital internally. And his experience running Markel’s capital allocation makes him a better equity investor. (It’s worth noting Gayner started at Markel managing the equity portfolio, then took over Markel Ventures – their private arm of business – and now runs the whole company. No wonder he has some of the most unique insights.)

The bottom line is this: capital allocation and investing go back and forth. The two skills feed each other.

Be curious. Not judgmental. You have to understand a business deeply enough to judge how its leadership spends its money. And that requires curiosity – real curiosity – not a checklist.

The Investor Who Only Buys from Owners

If Gayner approaches capital allocation from the inside out (as a CEO who also invests), Frank Fischer at Shareholder Value Management in Frankfurt approaches it from the outside in: as an investor who only buys from owners.

Fischer’s philosophy rests on four pillars, and the one that separates him from most value investors is what he calls “Business-Owner.” He doesn’t just want a cheap stock with a wide moat. He wants to know: who controls the check book? Is it a professional manager thinking in quarterly earnings cycles? Or is it an owner – a founder, a family, someone whose personal wealth is tied to the long-term health of the business?

This is not a soft preference. It’s a hard filter. Shareholder Value Management explicitly targets owner-managed or family-run businesses, because Fischer believes – and we concur – that the way a CEO allocates capital changes fundamentally when it’s their own money at stake. An owner thinks in decades. A hired manager thinks in bonus cycles.

Fischer calls his approach “Modern Value.” And the differentiator is the margin of alignment. Not only does he care about the fundamental value investing concept of margin of safety – he argues that when the person making the capital allocation decisions has their family’s wealth on the line, the quality of those decisions also tends to be very different. His firm’s motto captures it neatly: “Wir kaufen keine Aktien, wir kaufen überragende Geschäftsmodelle.” We don’t buy stocks; we buy outstanding business models. And the first thing they look at in any business model is who’s running it and how they spend the money.

The Mirror

Here’s what connects these two.

Gayner is a capital allocator who invests in other capital allocators. Fischer is an investor who only buys from owner-allocators. Different angle, same recognition: the skill that matters most in business is the one that’s hardest to find.

And both of them, independently, from different countries, different traditions, different fund structures, arrived at the same conclusion about what to look for. Not revenue growth. Not margins. Not even the moat (though they both care about moats). The thing they look for first is: does this person know what to do with a dollar?

There’s a reason this skill is so rare. Capital allocation requires you to be simultaneously curious and disciplined. Curious enough to see opportunities where others don’t. And disciplined enough to say no to the ones that feel exciting but don’t compound. It requires, in other words, exactly what Ted Lasso was talking about: the willingness to observe before judging. And to ask, “what is this?” before asking “what do I think about this?” (Trust me, it’s much harder than you think.)

That’s what Gayner does when he evaluates a Markel Ventures acquisition. That’s what Fischer does when he studies an owner-managed business in the Mittelstand. And honestly? That’s what we try to do at MAAT every single day.

-- Jenny Ngan, Head of Business Development